Coming Apart (Part II)

Divergent Paths

Part I: The Transatlantic Rift and the Divergent Social Structure of the US and Europe

By the early 1980s the period of temporary convergence between Europe and the United States (as well as the Anglosphere more broadly) had come to an end. The crisis of the 1970s had produced highly distinct results, as leaders in the Anglosphere sought out a radical break with the post-war system, while European leaders remained determined to preserve at least some of its most essential aspects. The neoliberal revolution reached the Old Continent only much later and in a significantly less radical form. This meant that the two societies would venture along drastically distinct paths from here on out, despite still retaining an incredibly close alliance for much of the next decades. Eventually, however, the socioeconomic divergence of this period would subvert that same alliance, as the two sides of the Atlantic came to view the other as alien and suspicious.

A Failed Break

The country which most notably chose a completely distinct path from the Anglosphere during the early 1980s was France, which chose to implement a programme diametrically opposed to the liberalisation overseen by Reagan and Thatcher. The crisis had produced a similar desire for a radical break with the status quo, but instead of betting on market liberalism France endeavoured on an ambitious programme of welfare state expansion and nationalisations. The “break with capitalism” Socialist President François Mitterrand had envisioned, however, soon turned into a complete disaster, burying any hopes of France establishing an alternative system to Anglo-Saxon liberalism. The main problem was massive capital flight and rapidly increasing inflation; the value of the French franc plummeted compared with other European currencies. This was especially problematic, as France was a member of the European Monetary System, which tied the value of the country’s currency to the German Deutschmark, only allowing for limited depreciations against that currency. Facing a choice between his domestic programme and his international credibility, Mitterrand abandoned the former, instituting the tournant de la rigueur (austerity turn) in 1983. Wages were frozen, spending curtailed, and many of the most ambitious nationalisations reversed. The supposed “French road to socialism” had led absolutely nowhere.

The failure of this programme had a number of profoundly paradoxical effects for the economic development of both France and the European continent as a whole. For one, it meant that France would actually mirror developments in the Anglosphere in one crucial way. Though it had already begun to deindustrialise in the 1970s, the process accelerated from this point onward. France would thus transition to a service-based economy faster than nearly any other Continental European country. The industrial sector would make up only 18% of French GDP in 2024, a share lower than even that of the US and UK, two countries which had made an embrace of the tertiary sector a core part of their economic strategy. This meant that the second-largest economy in Continental Europe was put into the unenviable position of massively losing industrial jobs without truly having a replacement industry. Structurally the French economy became broadly similar to the neoliberal Anglosphere, while retaining a developed welfare state, which kept it from developing the dynamism these countries exhibited during this era. Mass unemployment would become a permanent feature of the French economy from this point onward, a problem it came to share with much of the rest of the continent.

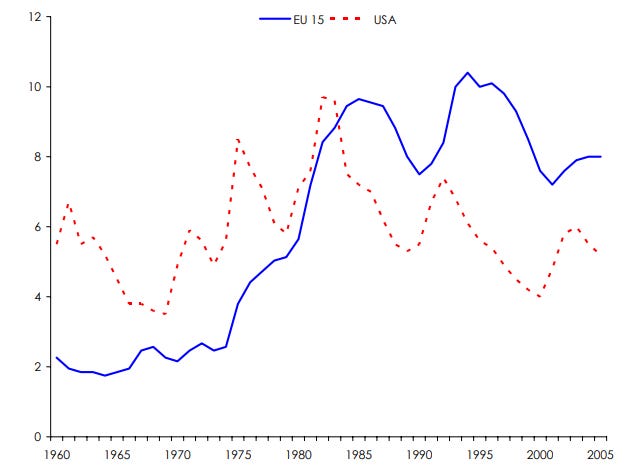

Different but Complimentary

In both the UK and US unemployment had peaked in either 1982 or 1983, but in Europe it continued to increase for the rest of the decade. Despite this persistent weakness, embracing the neoliberal revolution continued to be deemed politically unfeasible. The most significant figure in this regard was German Chancellor Helmut Kohl, who had come to power as a Conservative roughly concurrently with Reagan and Thatcher. But Germany, the country in which the modern welfare state had originated, had grown too used to the economic security offered by state intervention to embrace this radical break with the post-war consensus. This hesitancy to embrace radical reforms was reinforced by the fact that German industry had managed to exit the crisis of the 1970s relatively well. This meant that the country saw little incentive to actively embrace deindustrialisation, as the UK and US had done. Rather, the most advantageous path was deemed to remain wedded to the industrial model, betting on the country’s comparative advantage in this regard. The relative resilience of the country’s industry did not save it from the fate of elevated unemployment rates, however; by the mid-1980s unemployment in the country which had been the main beneficiary of the post-war boom regularly exceeded that in the Anglosphere.

The divergence in economic policy between the two societies during this period did not, however, produce any rift in the Transatlantic alliance. This primarily had two reasons: for one, the two societies were still tied together by their shared opposition to Soviet Communism. If anything, this period saw a renewed strengthening of the Transatlantic alliance, after some rifts had formed in the previous decades. The stressors of Vietnam, Neue Ostpolitik, and public backlash among European populations against the NATO dual-track decision had passed, with leaders such as Helmut Kohl once more unambiguously embracing the American President (who held his famous speech urging Soviet Premier Michael Gorbachev to “tear down this wall” in Germany during this period). A second major factor was that while the economic models during this period were highly distinct, they remained complementary. The Anglosphere’s decision to embrace deindustrialisation and the service sector meant that industrial goods had to be purchased somewhere else. This meant that demand for goods from the US’s major allies in the developed world massively increased. The leadership of Germany and Japan may have remained hesitant to embrace the US’s economic revolution, but they continued to gladly sell cars and household appliances to US customers. This meant that during this period a massive divergence in terms of trade balances began to form between the US and Continental Europe and Japan. While previously all major developed economies had alternated in running trade deficits and surpluses, now some countries turned into essentially permanent surplus countries. From 1976 onward the United States would not run a single trade surplus, with foreign countries accumulating massive amounts of dollar-denominated assets during this period. This sparked some consternation among US leaders, but measures to remedy the imbalance remained half-hearted. The Plaza Accord of 1985 saw leaders of Germany, France, the UK, and Japan agree to let their currencies appreciate in relation to the dollar, but this only brought a temporary respite for the US trade balance. The decision to shift economic policy away from industry left US manufacturing permanently uncompetitive with other developed economies. Firms such as Ford or GM continued to see their market share erode, as the heart of American manufacturing was increasingly transformed into the “Rust Belt”.

The increasing “globalisation” of economic output and supply chains was beginning to reshape the global economy. For the moment it was still largely contained within the developed economies allied with the US, as the Communist world remained excluded from Western supply chains, but its transformative effect for the world at large was beginning to become apparent. And this development was one which Continental Europe had much less qualms about embracing. In fact, supranational integration was seen as a tool to avoid the humiliation which economies such as France had to face during the previous decades. If authority over monetary policy could be delegated to a powerful international institution, elected leaders would never again have to be faced with a choice between domestic welfare and price stability. This calculation had rendered François Mitterrand, along with his previous finance minister Jacques Delors, one of the core figures pushing for another round of European integration. This push proved especially successful with regard to the creation of the Single Market (a project which was also enthusiastically supported by Margaret Thatcher), but was met with much more suspicion with regard to the creation of a single currency. German Chancellor Helmut Kohl especially remained sceptical, as the Mark was widely regarded as the ultimate symbol of German economic dominance. Whether Mitterrand would have succeeded in convincing him to establish a common currency, absent the rapid collapse of the empire which had dominated Eastern Europe and parts of Germany for the past four decades, remains a major mystery of European politics. What can be said with certainty is that the power whose expansion and potential dominance of the European continent had produced the Transatlantic alliance to begin with was about to collapse in absolutely spectacular fashion. And with it would collapse much of the raison d’être for the alliance between the US and Europe, the relationship never quite regaining its core sense of purpose.

Continued in Part III